If you came here looking for a Crunchbase entry, a Series A press release, or a list of venture funds with logos on the company’s website, you can stop scrolling. VUCA Solution — the Brazilian restaurant ERP behind vucasolution.com.br — has raised no outside capital. No seed round. No angels. No strategic checks. Nothing.

In a SaaS world that often treats fundraising announcements as a substitute for traction, that absence is worth a closer look.

What VUCA Solution Actually Is

VUCA is a vertical SaaS built specifically for the bar and restaurant segment in Brazil. Not a generic ERP with a “restaurant module” bolted on — the product was designed from the ground up for how kitchens, dining rooms, and delivery operations actually work. The platform covers front-of-house point-of-sale, inventory, purchasing and supplier quotes, financial controls and bank reconciliation, payroll, production, delivery, tip management, and real-time dashboards. There’s an iFood integration that automatically deducts ingredients from inventory when a delivery order comes in, and the company runs its own marketplace, Vuca Food.

It’s the kind of feature surface area that, in most pitch decks, gets used to justify a $10M Series A. VUCA built it without one.

The Funding Question — and Why It Matters

The Brazilian foodtech and restaurant-tech space has seen no shortage of capital over the last decade. Goomer, Saipos, Consumer, Cardápio Web, Cuoco, and others have all raised institutional rounds at various stages. Against that backdrop, a company operating in the same category with more than a thousand restaurant partners and a 10,000-follower Instagram presence — but no fundraising history — stands out.

So why does this matter to anyone outside the company?

Because “how much have they raised” has quietly become shorthand for “how serious are they?” — and that shorthand is wrong often enough that it deserves to be challenged. Capital raised is an input, not an output. It tells you how much runway a company bought. It tells you nothing about whether the product works, whether customers pay, or whether the unit economics make sense.

For a buyer evaluating a restaurant ERP, the more useful questions are: Does the software handle my actual operation? Will the company still exist in three years? Is the roadmap driven by what restaurants need, or by what the next investor wants to hear?

What Bootstrapping Looks Like in B2B Vertical SaaS

Bootstrapped vertical SaaS isn’t a novelty. Some of the most durable software businesses ever built — 37signals, Mailchimp before its acquisition, ATT Cobre, large parts of the accounting-software market — grew without venture capital. The pattern repeats because vertical SaaS rewards a specific set of behaviors that VC-backed playbooks tend to discourage:

Pricing for profit, not for growth charts. A bootstrapped company can’t afford to give the product away to inflate logo counts. It has to charge what the product is worth from day one, which forces the team to actually understand what the product is worth.

Building features customers ask for. Without a board pushing for the next “platform play,” product decisions stay closer to operator pain. The reason VUCA’s purchasing module has supplier quote-sharing and the inventory module ties to iFood deductions is almost certainly that restaurant owners asked for it — repeatedly — and somebody on the team listened.

Slower geographic expansion. This is a feature, not a bug. Restaurants are intensely local: tax rules, payment rails, supplier ecosystems, and labor regulations vary by country and sometimes by state. Companies that try to be everywhere at once usually end up half-built in every market. VUCA being Portuguese-only and Brazil-focused isn’t a limitation — it’s a strategy.

Survival as a strategic asset. Restaurant operators have been burned repeatedly by vendors that raised, scaled, pivoted, and either disappeared or got acquired into irrelevance. A company still around in five years using the same software you bought is worth more than a company with twice the features that disappears in eighteen months.

The Trade-offs Are Real

None of this is to romanticize bootstrapping. There are real costs:

A self-funded company can’t outspend a competitor on sales and marketing. If a well-capitalized rival decides to dump money into the same segment, the bootstrapped company has to win on product and word of mouth — and that takes longer.

International expansion, when and if it makes sense, is harder without capital. Building a second-language version of a Brazilian ERP is non-trivial.

Hiring competes with funded startups offering equity-laden packages. Bootstrapped companies have to sell candidates on the work itself and on profit-sharing rather than lottery-ticket equity.

And recessions or category downturns hit harder when there’s no war chest. The pandemic was brutal for restaurant tech, and bootstrapped vendors had to cut and survive on actual revenue — there was no “extend the runway” option.

The Number That Actually Matters

The honest answer to “how much has VUCA raised” is: R$0. The more interesting number — the one nobody puts in a headline — is how much revenue they’ve collected from paying restaurants over the years they’ve been operating. That’s the number that funds the development team, keeps the servers running, and decides whether the company is around in 2030.

You won’t find it on Crunchbase. You’ll find it in the fact that the product keeps shipping, the customer base keeps growing, and the company keeps showing up.

In a category littered with the corpses of well-funded restaurant-tech startups, that might be the more impressive metric.

Have you worked with bootstrapped vertical SaaS, either as an operator or a buyer? I’d be curious to hear how you weigh fundraising history when you evaluate vendors.

March 2026 looked like a month in which investors tried to hedge their existential dread with a mix of AI, insurance, healthcare and, for reasons only private equity can fully explain, eggs. The market served up a familiar cocktail: big names doubling down, founders attaching “AI” to anything with a pulse, and capital still showing up where distribution, defensibility, or regulation create real moats.

The vibe was less “spray and pray” and more “pick your spots, then write a real check.” Late-stage conviction showed up in insurtech, healthtech kept earning its seat at the table, and the seed market rewarded a few narratives that feel very 2026: stablecoins, AI-native platforms, and founder communities dressed as companies until proven otherwise. In other words, same circus, slightly better unit economics.

Deep Dive: Top 5 Most Relevant Deals

1) Global Eggs — Private Equity, USD 1B This is the deal nobody in venture can ignore, even if it technically wandered in from the neighboring private equity party. A billion-dollar round led by Warburg Pincus automatically bends the month’s gravity field; size alone puts it in a different solar system from everything else on the list. It is not the sexiest company in the file, but that is precisely the point: when that much capital goes into a deeply real, asset-heavy business, it reminds the ecosystem that “boring” industries with cash flow and scale still beat pitch-deck poetry in the capital stack.

2) Azos — Series C, USD 24.1M Azos made the cut because it checks every serious-investor box: meaningful round size, a long funding history, and a cap table stacked with real hitters. Kaszek and Kevin Efrusy led this round, while prior rounds brought in Lightrock, Munich Re Ventures, Prosus Ventures, MAYA and Propel—basically a roll call of people who do not wire money out of boredom. This is what maturity looks like in Brazilian insurtech: repeated institutional validation, sector specialization, and enough financing continuity to suggest the company is no longer selling vision alone; it is selling proof.

3) Mevo — Series B, USD 18.2M Mevo stands out because it combines scale, category relevance and repeat investor conviction in a way the market increasingly rewards. Floating Point led, with Matrix and Prosus on the cap table, and prior rounds show this is not a one-off enthusiasm spike but a multi-stage underwriting of the company’s role in digital healthcare. The detail that catches the eye is the back-to-back Series B cadence after a larger 2024 round: that usually signals a company still pressing the growth pedal while tightening the machine, not a tourist stop on the fundraising highway. Healthtech in LatAm still has plenty of PowerPoint merchants; Mevo looks more like operating infrastructure.

4) Saúde Bliss — Series A, USD 10.9M Saúde Bliss is one of the sharper ecosystem signals in the file because the round is not just reasonably large for a Series A; it also carries a very revealing investor mix. Banco Bradesco and K Fund led, with Canary, Clocktower and Speedinvest also involved, which gives the deal a useful blend of strategic validation, fintech sensibility and international venture credibility. In plain English: when incumbents and smart VCs both show up, it usually means the company has found a wedge worth respecting. Insurance comparison is not glamorous cocktail-party material, but in Brazil it sits close to distribution, trust and embedded financial services—three places where large outcomes like to hide.

5) shiva — Pre-Seed, USD 10M Shiva is the month’s most delightfully audacious line item: a pre-seed round of USD 10M led by Monashees, with Endeavor Catalyst participating, for a company described as a community supporting AI entrepreneurs. That sentence alone deserves both curiosity and a raised eyebrow. But that is exactly why it matters. The round is a bet on founder aggregation as an asset class and on AI-native company formation as something bigger than a software product. It may end up brilliant or absurd; the smartest March money seemed comfortable with the possibility that it is both. Either way, when Monashees writes that kind of early check, the ecosystem pays attention.

Honorable mention: BackChannel BackChannel narrowly missed the top five, but it has one of the strongest “smart money keeps returning” profiles in the file. Its USD 4.75M Series A followed two earlier seed rounds, with Sunna Ventures returning and a broad syndicate including Cathay, Norte, Positive, Preface, Accion and IGNIA-type names orbiting the company. That is not blockbuster-size capital, but it is exactly the kind of repeated institutional validation that often precedes a much louder round later.

My ranking leaned most heavily on four things from your file: absolute round size, repeatability of investor conviction across rounds, quality of the syndicate, and whether the company sits in a category with real ecosystem spillover rather than isolated niche appeal. On that basis, March/2026 looked like a month where the market rewarded businesses with either hard distribution moats or hard narrative momentum—and ideally both.

All deals March/2026

Deals Coverage Report | Period: March 2026 – March 2026

Core AI Simplifies credit with AI-powered tools for SaaS growth through seamless, customized solutions.

Lead Investors: 14B Venture Capital / Investors: 14B Venture Capital, André Street, BFF Ventures, big_bets, Eduardo Pontes, Fersen Lambranho, GP Investments, Nameless Partners, Norte Ventures

2026-03-12 / Nilo Saúde / Series A / USD 2,830,189

SaaS platform for LatAm healthcare payers and providers, that helps acquire, engage and navigate patients using AI and automation.

Lead Investors: Citrino Ventures, 14B / Investors: N/A

Previous Rounds

2022-01-31 / Series A / USD 11,200,000

Lead Investors: Global Founders Capital, Upload Ventures / Investors: Canary, Everywhere Ventures, Global Founders Capital, IKJ Capital, Lupa Capital, MAYA Capital, Tau Ventures, Two Culture Capital, Upload Ventures

2020-04-20 / Pre-Seed / USD 1,700,000

Lead Investors: Canary, MAYA Capital / Investors: 10K Ventures, Canary, Eretz.bio, Fernando Czapski, Grão, Guilherme Bonifacio, IKJ Capital, MAYA Capital

Azos is an insurtech that offers best in class insurance products in Brazilian market.

Lead Investors: Kaszek, Kevin Efrusy

Previous Rounds

2025-02-19 / Series B / USD 30,500,000

Lead Investors: Lightrock / Investors: Kaszek, Kevin Efrusy, Lightrock, MAYA Capital, Munich Re Ventures, Propel, Prosus Ventures

2022-05-18 / Series A / USD 6,000,000

Lead Investors: Munich Re Ventures / Investors: 4equity – Media Ventures, Airborne Ventures, Kaszek, Lupa Capital, Munich Re, Munich Re Ventures, Prosus

Data and Monitoring SaaS for Private Credit in Brazil

Lead Investors: Carlos Netto / Investors: Carlos Netto, Daniel Coquieri, João Baptista Peixoto Neto, Olavo Nigel Saptchenko Meyer, Omar Ajame, Paulo David, Vinicius Machado

February 2026 looked like a month when investors kept one hand on the spreadsheet and the other on the hype buzzer. There was real money deployed, but not in a spray-and-pray sort of way: capital clustered around fintech infrastructure, cybersecurity, and agtech—sectors with enough substance to survive after the AI glitter settles. If January wore a blazer over a T-shirt, February upgraded to loafers and started asking tougher questions about revenue quality.

The file also has a familiar venture quirk: tiny rounds with enormous ambition sitting right next to institutional checks that actually move the market. That contrast is the story. Some founders are still selling the future with admirable confidence; others are quietly becoming the companies that incumbents and late-stage investors can no longer ignore. As usual, the ecosystem loves a good narrative—but this month, capital was mostly chasing companies that had one.

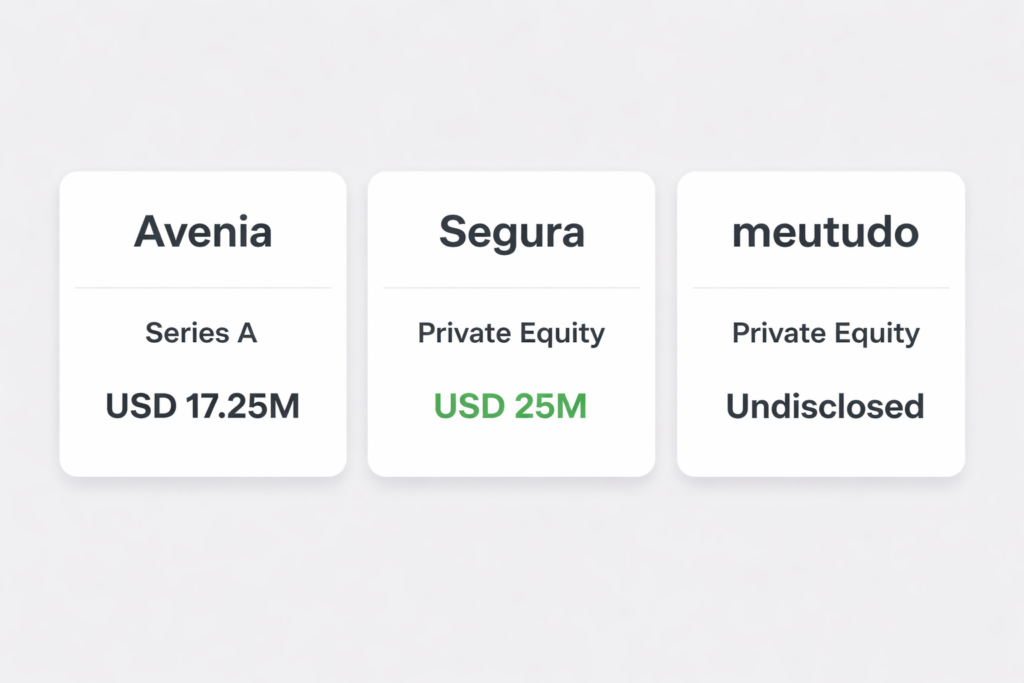

1. Avenia — Series A, USD 17.25M This is the cleanest “important venture deal” in the file. The round is large, the step-up from a roughly USD 2.1M Seed is dramatic, and the syndicate is stacked: Quona Capital and big_bets lead, with Sequoia Capital, Headline, Endeavor, Patria, Scale-Up Ventures, and others in the mix. The company is pitching itself as the “AWS for financial services” with stablecoin-powered FX—exactly the kind of infrastructure-meets-fintech story that gets sophisticated investors excited when the rails are more interesting than the app. This matters because it signals that Latin American financial plumbing is still one of the few places where big vision and real capital can coexist without everyone needing to pretend it is consumer social.

2. Segura — Private Equity, USD 25M By raw dollars, this is one of the month’s biggest disclosed checks, and the category gives it extra weight. Segura, formerly senhasegura, is already a recognized name in Privileged Access Management, which means this is not just another cyber startup hoping “zero trust” still sounds expensive enough. Riverwood Capital leading a USD 25M private equity round after a prior USD 13M Series A is a strong endorsement of both maturity and market position. For the ecosystem, it is a reminder that cybersecurity in Brazil can produce real scale—not just good decks and anxious CISOs.

3. meutudo — Private Equity, amount undisclosed An undisclosed round usually makes editors grumpy, but meutudo belongs here because significance can outweigh missing numerals. BTG Pactual leading a private equity round into one of Brazil’s most relevant credit platforms is a major institutional signal, especially given the company’s long arc from Seed backing by DOMO.VC, Bossa Invest, and BoostLAB into a much more mature financing event. This is not a novelty bet; it is a scaled fintech story entering the zone where large financial institutions start treating startups less like experiments and more like strategic assets. That is when the ecosystem stops calling you “promising” and starts calling your banker.

4. BEMAGRO — Series A, USD 5.8M BEMAGRO makes the list because it combines solid round size, repeat backing, and a strategically important sector. After two 2024 Seed rounds led by CNH Industrial and backed by corporate and ag-focused investors, the company returned with a USD 5.8M Series A led by Arara Seed and The Yield Lab LATAM, while keeping an impressively relevant syndicate that includes Positive Ventures, Suzano Ventures, and CNH Industrial. In plain English: this is agtech with grown-up backing, not just drone footage over soybean fields. It matters because Brazil continues to generate some of its most defensible venture cases where software meets the physical economy.

5. Ruvo — Seed, USD 4.6M Ruvo earns its slot because the round punches above its weight on investor quality. A USD 4.6M Seed is already meaningful, but the syndicate—1confirmation leading, with Coinbase Ventures and Y Combinator participating—puts this firmly in the “pay attention” category. The company is building a cross-border account layer connecting USD, BRL, Pix, crypto, and Visa, which lands squarely in the increasingly crowded but still important race to modernize money movement. Editorially, this is the kind of deal that says global crypto-fintech investors still see LatAm as fertile ground—provided the startup is solving a real payments problem and not just inventing a new token to celebrate having one.

February deals:

Deals Coverage Report | Period: February 2026 – February 2026

January 2026 felt like a month when venture investors tried to look disciplined while still sneaking out for a little speculative fun. The file is not packed with endless trophy rounds, but it does have a clear hierarchy: one genuinely large financing, a couple of strong follow-on rounds with respectable backers, and a few smaller checks where the investor name matters more than the amount. In other words, the market opened the year wearing a blazer over a T-shirt—serious enough for the LP meeting, casual enough to still say “AI-native” with a straight face.

The vibe, broadly, was selective optimism. Infrastructure, fintech, ag, and workflow software drew the most credible attention, while several smaller rounds looked more like option value than conviction. That is not a criticism; it is just the modern venture ecosystem doing what it does best: funding the future in uneven bursts, then pretending the pattern was obvious all along. January’s winners were the companies that either raised real money, attracted real investors, or managed to do both without hiding behind too much PowerPoint perfume.

1. UY3 — Venture round, USD 37.2M This is the undisputed heavyweight of the month. On round size alone, UY3 towers over the rest of the file, and the step-up from its June 2025 round of about USD 9.1M to USD 37.2M suggests meaningful momentum rather than a polite bridge dressed as growth capital. Vinci Compass leading adds institutional heft, and the company’s positioning in financial solutions and credit services gives it enough market relevance to matter beyond the spreadsheet. For the ecosystem, this is the kind of round that says capital is still available for fintech-adjacent infrastructure—provided you are building something more durable than a glorified cashback app.

2. Nagro — Series B, USD 9.3M Nagro earns its place because it checks every editorial box: meaningful size, clean stage progression, and credible investors. The company has gone from angel and pre-seed roots through Seed and Series A into a Series B led by Rabo Partnerships, with Itaú Ventures in the syndicate. That is serious validation in agfintech, a sector where thematic appeal alone is never enough—you need underwriting logic, distribution, and trust. This round matters because it reinforces a theme Brazil keeps producing: venture-scale companies built around real economy pain points. Ag is not always glamorous, but it does have the rude habit of mattering.

3. Lerian — Seed, USD 5.68M For a Seed round, this is a very respectable check, and the syndicate makes it more interesting. MAYA Capital is back after leading the prior USD 3.17M Seed, while Norte Ventures, Crivo, Supera, BluStone, and Kevin Efrusy deepen the credibility. More important, the company is in core banking infrastructure built on an open-source ledger—exactly the kind of plumbing-layer bet sophisticated investors like when they want exposure to fintech without buying the thousandth front-end neobank pitch. The relevance here is not just that Lerian raised money; it is that it raised again from people who understand the stack. That tends to be a better signal than founders using the phrase “modular banking” like incense.

4. Magie — Seed, USD 5M Magie makes the cut because the company combines a strong narrative with a strong repeat backer. Lux Capital led both the prior USD 3.93M Seed and this new USD 5M round, after Canary had backed the pre-seed, which tells you this is not random tourist money wandering through Latin America. The “WhatsApp’s first smart account” positioning gives it a high hype factor, but it is also aimed at a very real user behavior layer in Brazil and other messaging-first markets. Editorially, this matters because investors are clearly still willing to fund consumer-productivity hybrids when distribution logic feels native rather than imported. It is a reminder that sometimes the biggest interface in the market is not an app store—it is the green chat bubble everyone already lives in.

5. Camu — Venture round, amount undisclosed Normally, undisclosed rounds are annoying, because they ask editors to clap without showing the scoreboard. But Camu still belongs in the top five because Andreessen Horowitz is the lead investor, and that changes the conversation immediately. Even without an amount, a16z plus Everywhere Ventures behind a tax software company is not trivial; it suggests the company has both product ambition and enough category relevance to attract globally recognized capital into a deeply unsexy but mission-critical problem. And frankly, that is part of why it matters: taxes are the sort of pain point that founders rarely glamorize but customers never ignore. In venture, “boring but huge” has funded a lot more success than “viral but vague.”

A near miss is Anbetec Tecnologia, which raised a healthy USD 5.67M and sits in enterprise ERP infrastructure, but the investor signal is not quite as sharp as the five above. Aliado also deserves a nod for the AI-retail angle and the Headline backing, yet the round is smaller and the financing history less developed. Good companies, interesting rounds—just not the five that best define January’s actual power structure.

December 2025 had a very specific smell: less champagne-sprayed “to the moon” energy, more cold-eyed capital allocation with a side of AI seasoning. The list still has the usual startup zoo—voice agents, stablecoins, CRM, cloud, healthcare automation, and at least one company trying to make death planning sound user-friendly—but the real pattern is that bigger checks went to businesses with either institutional gravity or a story investors could explain without needing a 47-slide TAM deck.

In other words, December was not a month for cosplay venture. It was a month for grown-up rounds: late-stage companies proving they can still raise, breakout seeds pulling in brand-name funds, and a few category bets where the syndicate tells you more than the press release ever will. The market may still adore buzzwords, but this file suggests investors were at least pretending to read the fundamentals again—and, for once, some of them probably did.

1. Creditas — Series G, USD 108M This is the deal of the month, full stop. The round size is massive by any local standard, and the funding history reads like a greatest-hits album of LatAm fintech capital: Kaszek, QED, IFC, Prosus, SoftBank, Lightrock, Fidelity, and now another large round led by Andbank after it had already backed the 2022 Series F. That matters because this is not a speculative “AI for left-handed dentists” story; Creditas is one of the ecosystem’s true scaled fintech franchises, and a USD 108M Series G says serious investors still believe there is real enterprise value left to compound here. In ecosystem terms, this is the kind of round that reminds everyone that maturity is not a dirty word—especially when the cap table looks like an invite-only Davos side event.

2. Rivio — Seed, USD 18.1M A Seed round this large does not whisper; it kicks the door in. Rivio stands out because the check size is huge for the stage, and because Monashees and Valor Capital Group leading together instantly upgrades the signal quality, with Endeavor and Scale-Up Ventures reinforcing the syndicate. The company is attacking hospital management, waste reduction, and revenue cycle automation—exactly the kind of messy, expensive operating problem where software can create real value and where AI has more to do than merely write quirky LinkedIn posts. For the market, Rivio matters because it shows top-tier capital is still willing to underwrite ambitious healthcare infrastructure plays when the problem is painful enough and the founders make the math look credible.

3. EVEO Enterprise Cloud — Venture round, USD 18.27M EVEO is the sort of deal that may not dominate cocktail-party chatter but absolutely deserves editor attention. The round is large, the company sits in a real infrastructure layer—enterprise cloud and telecom services—and the lead is XP Asset Management, which gives the financing a more institutional flavor than the average early-stage raise. There is less visible prior-round color in the file than with some other companies, but sometimes the number itself tells the story: USD 18.27M is not angel-money dressed in a blazer. This matters for the ecosystem because it suggests investors are still willing to fund foundational picks-and-shovels businesses, not just whatever can squeeze “agentic AI” into the first sentence of the pitch.

4. Crown — Series A, USD 13.5M Crown makes the cut because this is where size, momentum, and pedigree line up almost suspiciously well. It raised USD 8.1M just two months earlier at Seed from Framework Ventures, with Coinbase Ventures, Paxos, Norte Ventures, and Valor Capital Group in the round, then followed with a USD 13.5M Series A led by Paradigm. That is not ordinary progression; that is the market saying, “we see something here, and we’d like to own more of it before everyone else catches up.” The company’s relevance goes beyond crypto fashion: a BRL-backed stablecoin issuer with compliance and liquidity as the pitch is pointed directly at a real financial infrastructure gap. This is one of the month’s clearest “small company, very big signal” rounds—and yes, when Paradigm shows up, people suddenly rediscover a philosophical interest in stablecoins.

5. Skyone — Series C, amount undisclosed Undisclosed rounds are often the venture equivalent of wearing sunglasses indoors, but Skyone still belongs in the top five because the lead investor is Advent International and the company has a long, credible financing history from Series A through multiple Series B rounds. When a global heavyweight like Advent leads a Series C, you do not need the exact number to know the company has crossed into a different class of relevance. Skyone matters because it is a reminder that enterprise software and cloud infrastructure can still produce late-stage conviction in Brazil, especially when the business has shown enough durability to attract both strategic and institutional money over time. Translation: not every big outcome has to come wrapped in fintech swagger or crypto vocabulary.

One near-miss worth noting is Clara: the December round itself is tiny, but the company’s broader funding history—General Catalyst, DST, Coatue, Kaszek, Monashees, Citi Ventures, GGV—remains elite. It did not make the top five because this exercise is about the month’s most relevant deals, not just the most famous names in the file. Still, whenever a company with that kind of cap-table gravity appears, even in miniature, the market pays attention.

Hablla is a conversational marketing and CRM platform unifying omnichannel business communication.

Lead Investors: Bossa Invest

Previous Rounds

2024-04-12 / Seed / USD 166,064

Lead Investors: Bossa Invest

2025-12-22 / Clara / Venture – Series Unknown / USD 267,568

Clara is a spending management company that provides an end-to-end spend management platform for businesses.

Lead Investors: Gaingels / Investors: Gaingels, Sahin Boydas

Previous Rounds

2025-04-29 / Venture – Series Unknown / USD 40,000,000

Lead Investors: Citi Ventures / Investors: Citi Ventures, Citius, Coatue, DST Global, Kaszek, MONASHEES, Notable Capital, Pathlight Ventures

2024-12-31 / Venture – Series Unknown

Lead Investors: Michele Attisani

2024-04-16 / Venture – Series Unknown / USD 3,500,000

Lead Investors: General Catalyst / Investors: Adapt Ventures, Canary, General Catalyst, Picus Capital

2023-04-26 / Series B / USD 60,000,000

Lead Investors: GGV Capital / Investors: Acrew Capital, Alter Global, Bayhouse Capital, Citi Ventures, Citius, Coatue, Commerce Ventures, DST Global, Endeavor Catalyst, Ethos VC, Evolution Ventures, Fluent Ventures, General Catalyst, GGV Capital, Goanna Capital, Grey Wolf, Lago Innovation Fund, MONASHEES, Picus Capital

2021-12-06 / Series B / USD 70,000,000

Lead Investors: Coatue / Investors: Adapt Ventures, Alter Global, Avid Ventures, BoxGroup, Coatue, DST Global, Gaingels, General Catalyst, Global Founders Capital, ICONIQ Growth, MONASHEES, Picus Capital, Sahin Boydas

2021-07-21 / Series A / USD 5,000,000

Lead Investors: Andy Cohen / Investors: Andy Cohen, Antonia Rojas Eing, Ariel Lambrecht, Brendan Dickinson, Brynne Rojas, Daniel Vogel, Deepak Chugani, German Peralta, Hans Tung, Howard Han, Manolo Atala, Max Burger, Michael Levinthal, Oliver Jung, Philippe Teixeira da Mota, Picus Capital, Ricardo Weder, Sebastian Castro, Sebastian Kreis, Sebastian Mejia, Sebastian Villarreal, Sergio Furio

2021-05-26 / Series A / USD 30,000,000

Lead Investors: DST Global / Investors: Alter Global, Avid Ventures, DST Global, General Catalyst, Kaszek, MONASHEES

2021-03-10 / Pre-Seed / USD 3,500,000

Lead Investors: General Catalyst / Investors: Adapt Ventures, Alejandro Galvez, Brian Requarth, Canary, David Vélez, Eric Glyman, General Catalyst, Global Founders Capital, JAM Fund, Justin Mateen, Karim Atiyeh, Liquid 2 Ventures, Nicky Goulimis, Picus Capital, Soma Capital, SV Angel, Travis Foxhall, VentureSouq

FlowCredi runs a marketplace that links lenders and borrowers and provides credit products backed by real estate.

Lead Investors: Norte Ventures, VERVE CAPITAL / Investors: Gabriel Lacombe, Leandro Abreu, Norte Ventures, Patrick Sigrist, Rafael Duton, VERVE CAPITAL

Lastlink is an application which helps to monetize private and Telegram groups through subscription.

Lead Investors: Astella / Investors: Astella, BTG Pactual, Scale-Up Ventures

Previous Rounds

2023-03-30 / Seed

Lead Investors: BoostLAB

2021-07-01 / Pre-Seed / USD 1,400,000

Lead Investors: Canary / Investors: Canary, Graph Ventures, Gustavo Caetano, Israel Salmen, Marcela Rezende

2025-12-01 / The Led / Private Equity / USD 28,000,224

THE LED delivers complete packages with implementation, support, and multi‑sector applications in LED panel solutions.

Lead Investors: Kinea Investimentos Ltda

2025-12-01 / Creditas / Series G / USD 108,000,000

Creditas is a consumer loaning startup that operates a digital platform providing secured loans and low interest rates.

Lead Investors: Andbank

Previous Rounds

2022-07-07 / Series F / USD 50,000,000

Lead Investors: Andbank

2022-07-07 / Convertible Note / USD 150,000,000

Lead Investors: N/A

2022-01-25 / Series F / USD 260,000,000

Lead Investors: Fidelity / Investors: Actyus, Fidelity, Greentrail Capital, Headline, Kaszek, Lightrock, QED Investors, SOFTBANK Latin America Ventures, SoftBank Vision Fund, Sunley House Capital Management, VEF, Wellington Management

2020-12-18 / Series E / USD 255,000,000

Lead Investors: Lightrock / Investors: Amadeus Capital Partners, Headline, Kaszek, Lightrock, SOFTBANK Latin America Ventures, SoftBank Vision Fund, Sunley House Capital Management, Tarsadia Investments, VEF, Wellington Management

2019-07-10 / Series D / USD 231,000,000

Lead Investors: SoftBank / Investors: Amadeus Capital Partners, Mouro Capital, SoftBank, SoftBank Vision Fund, VEF

2017-12-11 / Series C / USD 50,000,000

Lead Investors: VEF / Investors: Amadeus Capital Partners, Bossa Invest, Endeavor Catalyst, International Finance Corporation, Kaszek, Mouro Capital, Prosus, QED Investors, Quona Capital, VEF

2017-02-21 / Series B / USD 19,000,000

Lead Investors: International Finance Corporation, Prosus / Investors: International Finance Corporation, Kaszek, Prosus, QED Investors, Quona Capital, Redpoint eventures

2016-06-20 / Series A / USD 4,500,000

Lead Investors: Kaszek, Redpoint eventures / Investors: Kaszek, QED Investors, Quona Capital, Redpoint eventures

2015-08-03 / Series A / USD 3,000,000

Lead Investors: Redpoint eventures / Investors: Headline, QED Investors, Quona Capital, Redpoint eventures

2013-10-18 / Seed / USD 1,400,000

Lead Investors: Napkn Ventures / Investors: Napkn Ventures, Rockaway Capital

November 2025 did not look like a broad risk-on month; it looked like a selective conviction month. The dataset is dominated by smaller seed, pre-seed, and unpriced venture rounds, but a handful of financings clearly stand above the pack because they combine meaningful capital formation with stronger signaling power from syndicate quality, round progression, and category relevance. In other words, the month was less about volume and more about which companies were still able to attract serious capital and credible backers.

What matters editorially is that the standout deals span very different parts of the ecosystem: vertical HR/logistics infrastructure, fintech-enablement software, B2B commerce rails, smart infrastructure, and late-stage fintech recapitalization. That mix suggests capital was still available in Brazil and LatAm-adjacent tech, but it was being deployed with discipline: toward companies showing either scale, resilience through multiple rounds, or unusually strong investor endorsement.

AI platform that serves as a factory for accountants and a steering tool for their clients

Lead Investors: Next Billion Ventures / Investors: Hedosophia, International Finance Corporation, MONASHEES, Next Billion Ventures, Valor Capital Group

Previous Rounds

2024-09-25 / BHub / Series A / USD 13,515,732

Lead Investors: International Finance Corporation / Investors: International Finance Corporation, Latitud, MONASHEES, Valor Capital Group

2022-09-13 / BHub / Series A / USD 7,705,828

Lead Investors: Moore Capital / Investors: BFF Ventures, MONASHEES, Moore Capital, Norte Ventures, Picus Capital, Scale-Up Ventures, Valor Capital Group

2021-12-14 / BHub / Series A / USD 20,800,000

Lead Investors: MONASHEES, Valor Capital Group / Investors: Clocktower Technology Ventures, Equitas Capital, Hedosophia, MONASHEES, Norte Ventures, Picus Capital, QED Investors, Scale-Up Ventures, Valor Capital Group

2021-09-22 / BHub / Seed / USD 4,400,000

Lead Investors: MONASHEES, Valor Capital Group / Investors: 17Sigma, BoostLAB, Clocktower Technology Ventures, EquitasVC, Latitud, Lee Fixel, MONASHEES, Norte Ventures, Picus Capital, QED Investors, Valor Capital Group

2021-11-17 / CloudWalk / Series C / USD 150,000,000

Lead Investors: Coatue / Investors: A-Star, Coatue, DST Global, Gokul Rajaram, HIVE Ventures, Kelvin Beachum Jr., Larry Fitzgerald, Plug and Play, Valor Capital Group

2021-05-11 / CloudWalk / Series B / USD 190,000,000

Lead Investors: Coatue / Investors: Coatue, DST Global, FIS, Plug and Play, The Hive, Valor Capital Group

Founders Fund and Sequoia Lead $35M Round in Brazilian Legaltech Enter

Brazilian legaltech Enter has raised $35 million in a round co-led by Founders Fundand Sequoia Capital, reaching a valuation of around R$ 2 billion (≈ US$ 350 million). The round also included Atlantico and ONEVC, highlighting growing investor confidence in Brazil’s artificial-intelligence ecosystem.

Enter uses AI to deliver auditable and reliable legal drafting for large companies and law firms, helping automate tasks such as case analysis, document generation, and litigation management. In a country with nearly 80 million ongoing lawsuits, the company’s technology promises to reduce costs and accelerate workflows in one of the world’s most complex legal systems.

The startup already works with major enterprises including Itaú, Santander, Mercado Livre, Nubank, and Airbnb, and expects to handle around 250,000 lawsuits this year alone.

This investment is significant for several reasons. It marks Sequoia’s second AI investment in Brazil, following its participation in Avra, and brings Peter Thiel’s Founders Fund back to the region—both funds were early backers of Nubank, now Latin America’s most valuable fintech. Their renewed interest signals that Brazil’s AI startups are entering a new phase of global relevance.

Beyond its valuation milestone, Enter’s round underscores how AI-driven vertical solutions—in this case, legaltech—are becoming central to Latin America’s innovation story. For global and local investors alike, the deal suggests Brazil is no longer just producing consumer-focused startups, but also deep-tech companies capable of solving structural inefficiencies in traditional industries.

Enter’s success may well open the door for a new generation of AI companies emerging from Brazil’s vibrant tech scene.

Infleet Raises $7.54M to Scale AI + IoT in Fleet & Logistics Hub

Brazilian startup Infleet, which offers a logistics and equipment management integration hub, has secured USD 7,538,920 (≈ R$ 40 million) in a Series A round led by Canary, Citrino Ventures, and Indicator Capital. Other participants include BluStone, DOMO.VC, and Scale-Up Ventures.

Infleet combines IoT sensors, real-time connectivity, and AI analytics to bring transparency, predictive insights, and operational agility to fleets. Its platform monitors driver behavior, vehicle condition, and usage patterns, enabling cost control, preventive maintenance, and risk reduction.

The Brazilian logistics market remains heavily truck-dependent: most goods move by road, and fleet operators face huge cost pressures, regulatory complexity, and fragmentation. Infleet’s growth addresses a critical infrastructure bottleneck in Brazil’s supply chain.

The startup has been growing at breakneck speed—reporting 120 % year-over-year growth, having expanded 50× since inception, and projecting similar momentum into 2025–2026.

With the new capital, Infleet plans to accelerate development of its “Intelligent Copilot” — a proactive assistant that alerts drivers to risk (e.g. fatigue, speed, distraction) while surfacing strategic dashboards and cost levers for fleet managers.

This funding round signals growing investor confidence in Latin America’s infrastructure software layer. Infleet represents more than a logistics play: it exemplifies how IoT + vertical AI can modernize foundational industrial systems that rarely draw attention — until inefficiencies become crippling.

As Brazil seeks productivity gains across supply chains, Infleet may become a key enabler of smarter, safer, and more sustainable transport operations across the region.

Omie Secures $158M in Landmark Deal, Brings Global Growth Capital to Brazil

São Paulo — In one of the most significant Brazilian startup financings of 2025, Omie, a cloud ERP/CRM software provider for small and medium enterprises, has raised USD 158,233,705 in a round led by Partners Group.

As part of the transaction, Partners Group acquired approximately 15 % of Omie for USD 100 million, valuing the company at around USD 700 million. The deal included a secondary component, allowing early investors (e.g. SoftBank, Riverwood, Astella) to partially exit while continuing to hold positions.

Omie, founded in 2013, has built a highly capital-efficient growth trajectory. Over 11 years, it has raised modest amounts relative to peers, yet matured into a stable SaaS operator serving more than 180,000 customers with 30–40 % annual growth, processing USD 6.5 billion in monthly invoices, and achieving cash-flow positivity since mid-2023.

This raise is a milestone for Brazilian tech: it marks Partners Group’s first growth equity investment in Brazil, and underscores the renewed appetite for Latin America’s scale-stage SaaS companies. Omie’s strong fundamentals and efficiency make it a poster child for how discipline and product leverage can attract global capital into Brazil’s SME infrastructure space.

In a market often dominated by high-risk bets, Omie’s rise shows the power of sustainable growth, deep vertical focus, and leveraging accounting channels to penetrate under-digitalized small business segments.